For retirement planning, you must apply a long-term perspective with goals that are decades away. You also need to be prepared to revise your tactics as you go, moving money into different savings vehicles and adjusting your retirement goals based on changes in your income and other factors.

The simple rule is that you will need at least 70% of your current annual income. That number is based on several assumptions, such as support from Social Security, using Medicare instead of paying for medical insurance, downsizing your home, paying less in taxes, and so forth.

Perhaps the biggest savings will be that you no longer have to save for retirement. However, there may also be added expenses, such as healthcare, travel, and so on. Consider 70% of your current income as the minimum amount you will need. You will also have to estimate the length of your retirement (e.g., do you plan to live to be 100 years old?).

It’s important to establish a retirement savings goal. You can use that goal as a benchmark to determine if you are saving enough or saving too little. You may also want to plan to adjust that goal as your financial circumstances change.

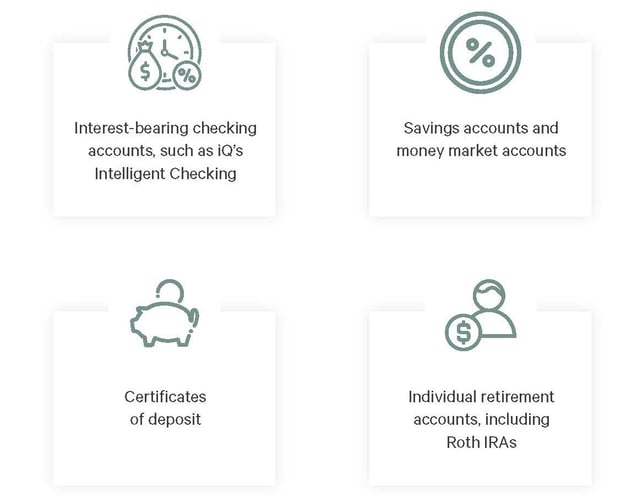

There are many ways to save for retirement. We already discussed the most common employment-backed retirement plans, such as 401(k) and pension plans. In addition to retirement savings from your paycheck, you should include other types of savings.

IRAs are the most common type of retirement savings plan. Traditional IRAs allow an individual to put up to $6,000 per year in a tax-deferred account; this increases to $7,000 per year if you are 50 or older. Contribution limits increased to $6,500— $7,500 for those 50 and up—in 2023. While an IRA can be beneficial for taxes—since it is tax-deferred, it can reduce your taxable income—you have to pay taxes when you use the money after retirement.

A Roth IRA differs from a traditional IRA because the money is taxed when you deposit it. In other words, the money you put away in a Roth IRA today is considered part of your taxable income, but the money is tax-free when you retire since the taxes have already been paid. Roth IRAs can offer a real tax advantage when you want to minimize your income taxes in your retirement years.

Remember that the overarching strategy for retirement is to start saving as soon as possible and diversify your savings to get the best return on your money. Talk to a financial advisor or wealth management professional about the best ways to make your money grow. For example, the stock market has yielded an average of 10% returns annually over the last century, which is a better return than you will see from a savings account or IRA.

However, where money put into a savings or IRA account is insured by the federal government, stock investments are not protected, so they are at higher risk. In addition, if you choose the wrong investments, you could lose money rather than make money. That’s why you want to diversify; spread your retirement money across different plans and accounts to make the most money you can with minimal risk.

And be sure to check the progress of your retirement savings regularly. Talk to your financial advisor about your retirement plan and see where you stand against your retirement goals. You may want to consider putting more money away or moving your money into different types of savings accounts to improve your return on investment.

What are the common types of savings options for retirement?

There are a variety of types of savings options designed specifically for retirement. Here is a list of the most common retirement plans:

-

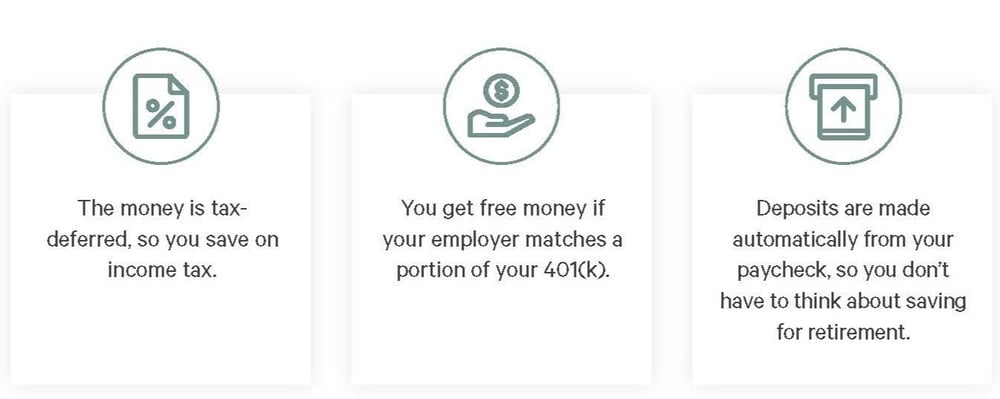

401(k): A 401(k) is a profit-sharing plan that defers a portion of your salary as taxable income. The income becomes taxable upon retirement. Employers often provide matching funds.

-

IRA: A traditional IRA allows you to set aside up to $6,000 per year or $7,000 if you are over age 50 as tax-deferred money for retirement. This contribution limit is $6,500—$7,500 for contributors ages 50-plus—as of 2023.

-

Roth IRA: Unlike a traditional IRA, a Roth IRA is not tax-deductible. Since Roth IRA contributions are counted as income, the tax is already paid, so withdrawals are not taxable when you retire. Some people choose to use Roth IRAs to reduce their taxable income when they retire.

-

SEP IRA: An SEP IRA allows employers to contribute to employees’ traditional IRAs. Although any business can set up a SEP IRA, it’s ideal for self-employed workers.

-

Investment accounts: Stocks, bonds, mutual funds, and similar investments can yield higher returns than other savings vehicles. They pose a greater risk since you can lose money and losses are not insured. Talking to a financial advisor about including investments in your retirement strategy is best.

Ready to take the power of smart saving a step further?

With an iQ Intelligent Savings account, you’ll unlock a new way to grow your funds—effortlessly. If you’re interested in exploring a uniquely high-yield way to save, check out Intelligent Savings, only available at iQ Credit Union.