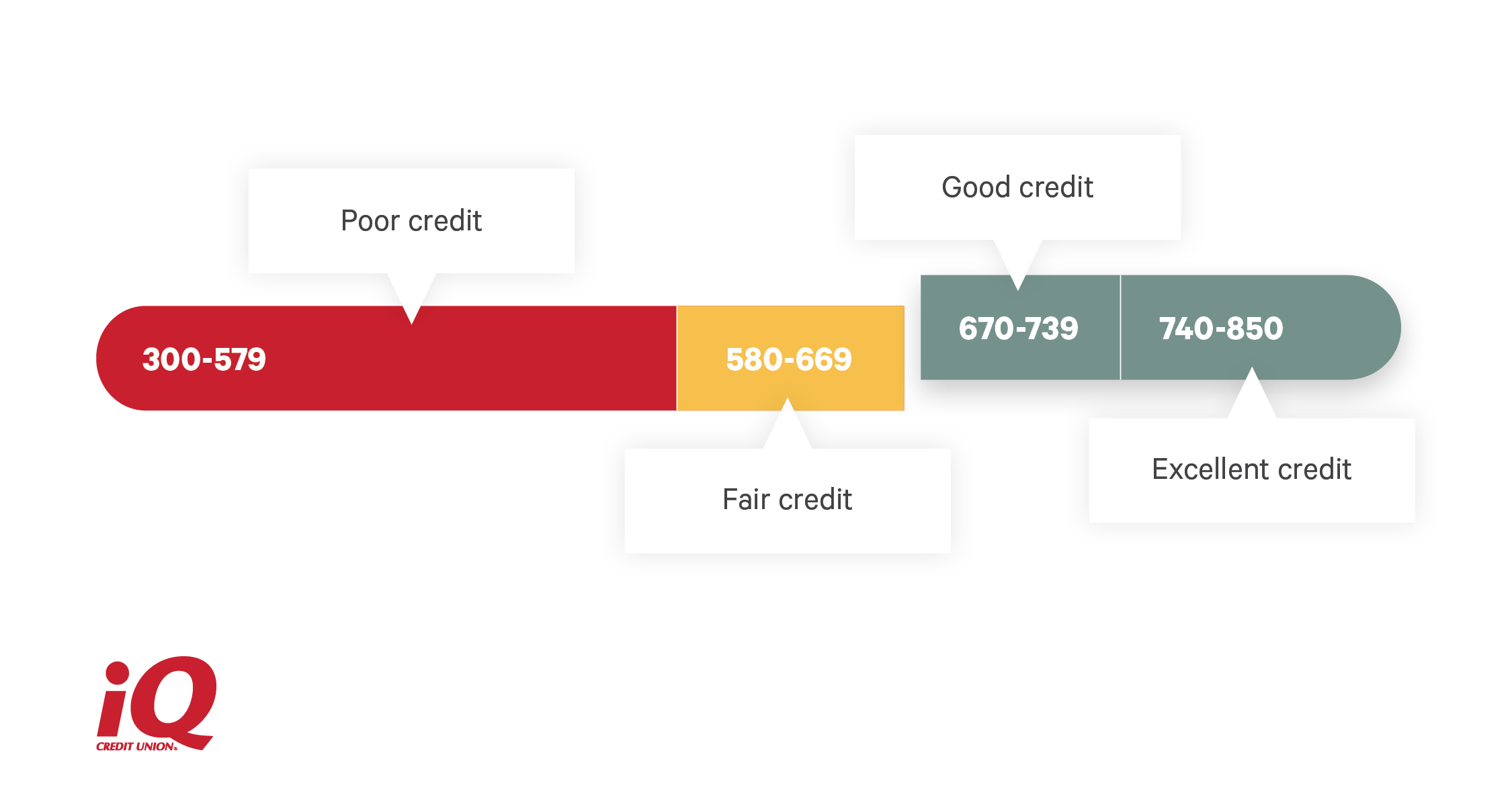

Once you start to establish your credit, you will find that there are times when having a good credit score can be very helpful. Chances are that you will need to borrow money at some point to finance a car purchase, buy a home, or pay an unexpected expense. Having good credit makes it easier to get the best loan you need, and it can help you get better loan rates because a higher credit score shows you are a good credit risk.

Borrowing to fund certain expenses or life events is quite common, even expected. Student loans, for example, have become commonplace for paying college tuition, and buying a home requires a home loan. There are times in your life when having good credit really counts:

Getting a Credit Card

With good credit, you can qualify for different types of credit cards, including cards that have low interest rates and that offer reward points, airline miles, and even cash back. The better your credit, the higher your credit card spending limit and the better your credit terms. iQ Credit Union offers different credit cards to meet every credit need, including a Visa Platinum card, a Visa Platinum Rewards card that offers 1% cash back on all purchases, and a Visa Signature Rewards card that provides one point for every dollar with extra points awarded for dining and travel.

Applying for a Home Loan

When you are ready to buy your first home, you are going to have to prove your creditworthiness in advance and show you can qualify for a mortgage before you will be considered a serious buyer. The first step for anyone shopping for a new home is to be prequalified for a home loan. By working with your bank, credit union, or mortgage broker, you can determine the size of your mortgage and what you can afford to pay for a home based on your credit and your income. The better your credit, the more you can afford and the better the terms you can negotiate on your home loan.

Taking Out a Car Loan

Very few people pay cash for a car, especially if they are just starting out, so you will have to take out a car loan. Even if you decide to lease a car instead of buying one, you still need to qualify for the lease, just as you would have to qualify for an auto loan. The better your credit, the easier it will be to negotiate a loan that suits your budget.

Qualifying for a Personal Loan

Sometimes you need extra cash for something unexpected, such as medical bills or an unexpected trip. In these cases, a personal loan might come in handy. With a personal loan, you are borrowing money solely on your good credit. Your credit score and credit history are the only indicators to the lender that you will repay the loan.

Navigating Debt

In addition to managing your credit so you can borrow money, you also have to manage your debt so you don’t get into financial trouble. If you don’t keep an eye on your spending and your debt, it is easy to become overextended with credit card payments or loan payments that take too much out of your household budget. If you do start to accumulate too much debt, there are steps you can take to get your debt back under control.

Debt consolidation is a common strategy. When you consolidate your debt, the idea is to reorganize your debt, taking credit cards, loans, and other outstanding debt with high interest rates and paying it off with a new loan or credit card at a lower interest rate. The concept is that by restructuring your debt at a lower interest rate, you will pay less money in the long run, and you can make the monthly payments more manageable.

One of the factors that affects your credit score is using too much of your available credit. This is defined as your debt-to-income (DTI) ratio: the difference between what you owe each month versus what you earn. If your DTI is too high, it is an indication that you are carrying too much debt and may have trouble repaying what you own.

However, you can carry a healthy amount of debt to show you are a responsible borrower. Financial experts recommend applying the 28/36 rule when budgeting for debt. The 28/36 rule says to spend no more than 28% of your total income on housing expenses, such as your mortgage, and no more than 36% of your monthly income on total debt, including housing, car loans, and credit cards. If you find that you owe between 43-50% of your monthly income in debt, it is time to take action to reduce your DTI.

Student loan debt presents a unique problem for many borrowers. Student loans are the second-biggest form of personal debt after mortgages, and 75% of students who took out loans did so to attend two- and four-year colleges. At the beginning of 2021, the average student loan debt for graduates of the class of 2019 was calculated to be almost $30,000 per student. To manage student loans as part of your overall debt, consider applying the 50/3o/20 rule developed by Senator Elizabeth Warren, which says to allocate 50% of your income for needs, 30% for wants, and 20% for savings. Student loans and other debt falls in the needs category, along with housing, food, utilities, and other essentials.

It also pays to plan for the unexpected. Research shows that only 39% of Americans have enough money set aside to pay for a $1,000 emergency. Even with an emergency fund that could cover three or even six months of household expenses, a major emergency such as a trip to the hospital can trigger financial disaster. The average three-day hospital stay costs $30,000. Having good credit can help you borrow money or arrange payments for healthcare. You also might consider opening a tax-advantaged Health Savings Account (HSA) to save money for medical expenses that aren’t covered by health insurance.

A financial tool that many people use so they have extra cash when they need it is a personal line of credit or home equity line of credit (HELOC). A line of credit is a form of revolving credit: Your bank or credit union extends an amount of money that you can tap when you need it and pay back over time, with interest, much like a credit card. A HELOC often gives you a larger amount of credit than a personal line of credit because the lender is using the equity in your home to guarantee the loan.